Technological pathways for cost-effective steel decarbonization

Article Date: 29 October 2025

Source: https://www.nature.com/articles/s41586-025-09658-9

Image: Figure 1

{kind=link}

Summary

This Nature study develops NZP-steel, a plant-level model that maps least-cost decarbonization pathways for nearly 1,967 major iron and steel plants worldwide across 2020–2050. The authors compile plant-level production and cost data, forecast dynamic costs for 20 promising decarbonization technologies using component-based learning and learning curves, and test three policy deployment scenarios (early, medium and late). Key findings: energy-efficiency upgrades (BAT for BF–BOF) are cheap and often cost-saving in the near term; Scrap–EAF is a mature near-zero option but limited by scrap supply; smelt reduction with CCS and hydrogen-based DRI routes become competitive in different regions over time; and a medium deployment strategy (use transitional low-carbon options, then zero-carbon) is the most cost-effective global pathway.

Key Points

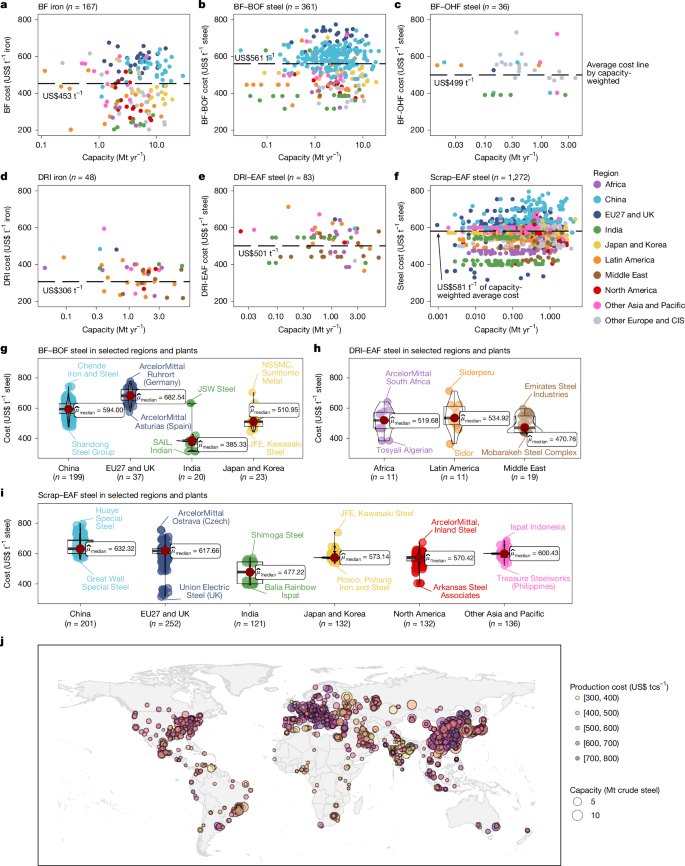

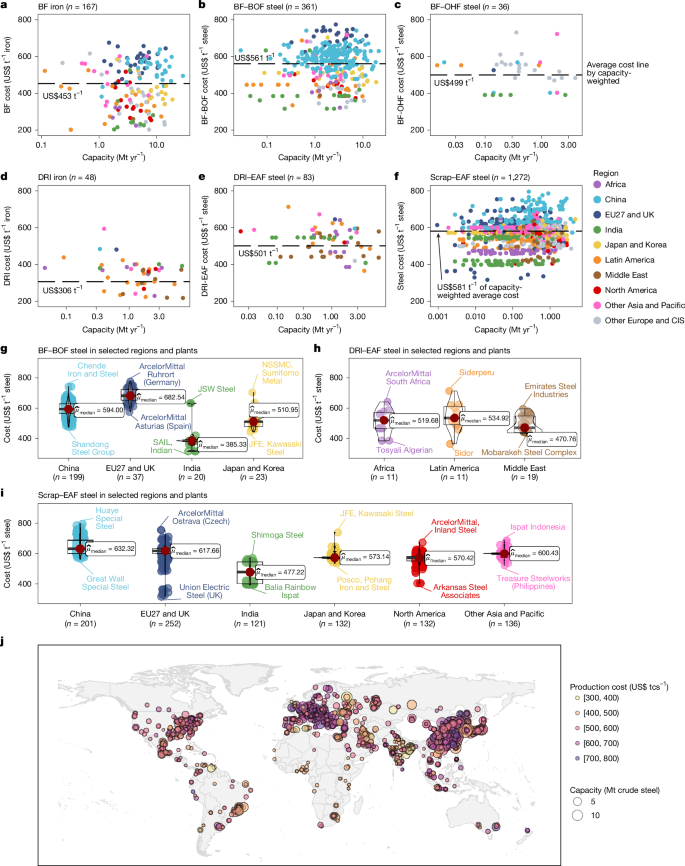

- The iron and steel sector produced ~2.8 GtCO2 in 2021 and is responsible for ~7% of global CO2 emissions; plant-level heterogeneity is large.

- NZP-steel is a plant-by-plant optimisation model integrating bottom-up plant costs and top-down national targets to identify least-cost retrofitting choices (retrofitting every ~20 years).

- A toolbox of 20 technologies was modelled; short-term cheapest wins are efficiency measures (BAT BF–BOF), while long-term zero-carbon choices include SR–BOF + CCS and DRI with green hydrogen or electrified routes.

- Scrap–EAF is the only broadly mature near-zero technology with low cost but growth is strictly limited by scrap availability.

- Under the medium deployment scenario global emissions fall to 1.1 GtCO2 in 2050 (from 2.8 Gt in 2020); cumulative abatement 2020–2050 = 22.4 GtCO2 at an average abatement cost of US$24.7 tCO2−1.

- The medium scenario is more cost-effective than forcing immediate zero-carbon deployment (early) or allowing late action: it balances transitional low-carbon options and eventual zero-carbon switches.

- Plant-level results show wide variation in abatement costs; many plants can reduce emissions at low or negative cost by adopting mature efficiency measures.

- Deep decarbonisation will require major finance (hundreds of billions US$) and policy incentives to avoid plant closures and stranded assets.

Content summary

The paper starts by documenting global plant heterogeneity: about 1,967 plants account for 98% of iron and crude-steel production and 80–90% of sector emissions. Unit production costs and CO2 intensity vary regionally and by plant age, scale and feedstock. Using two plant-level datasets (production and costs) and a component-based cost-forecasting method, the authors estimate dynamic, plant-specific costs for 20 decarbonisation options.

They test three policy deployment scenarios: early (zero-carbon from first retrofit), medium (use low-carbon transitional options first, then zero-carbon by final retrofit), and late (defer until final retrofit). Results show all scenarios cut emissions substantially by 2050, but the medium scenario delivers the best balance of abatement and cost: cumulative 22.4 GtCO2 at US$24.7 tCO2−1 versus 13.5 Gt at US$26.0 tCO2−1 (late) and 52.7 Gt at US$54.0 tCO2−1 (early). Regionally, China can rely heavily on CCS and increased scrap use; the EU can leverage green hydrogen; India will need earlier action to avoid steep post-2050 mitigation burdens.

Crucially, mature energy-efficiency upgrades (BAT BF–BOF) can abate ~7.8 GtCO2 cumulatively at negative average costs (around −US$8.5 tCO2−1) and thus represent ‘low-hanging fruit’. Where scrap is available, Scrap–EAF yields negative abatement costs in some regions. The paper emphasises sensitivity to input prices, learning rates and cumulative capacities (notably for CCS, hydrogen and electrolysers), and underlines the need for targeted finance to support transitions in less-profitable plants.

Context and relevance

This work is timely for policymakers, steel producers, investors and supply-chain actors because it moves beyond sectoral averages to actionable, plant-level decarbonisation routes. By combining cost forecasts, technical readiness and national net-zero constraints, the study shows which technologies are likely to be most cost-effective where and when. The finding that a medium-paced deployment (use mature low-carbon options as a bridge) minimises costs has direct implications for climate policy design, industrial support schemes and public funding priorities. The dataset and code released with the paper enable granular planning and targeted incentives to avoid stranded assets while meeting climate goals.

Why should I read this?

Short version: if you care about cutting industrial emissions without bankrupting steelmakers, this paper gives the playbook. It reads like a practical handbook — who should switch to scrap, where CCS pays off, when green hydrogen becomes affordable, and why simple efficiency upgrades are high-value now. Handy if you’re a policymaker, plant manager or investor who wants to know where to put money and when.

Author style

Punchy. The authors lay out a plant-by-plant roadmap rather than abstract sectoral targets — this is actionable research. If you work on industrial decarbonisation, procurement, infrastructure planning or climate policy, the detail here is significant: it shows how different policy timings and financing choices change both emissions and costs globally.

Source

Source: Technological pathways for cost-effective steel decarbonization — Nature (Wu et al., 2025)